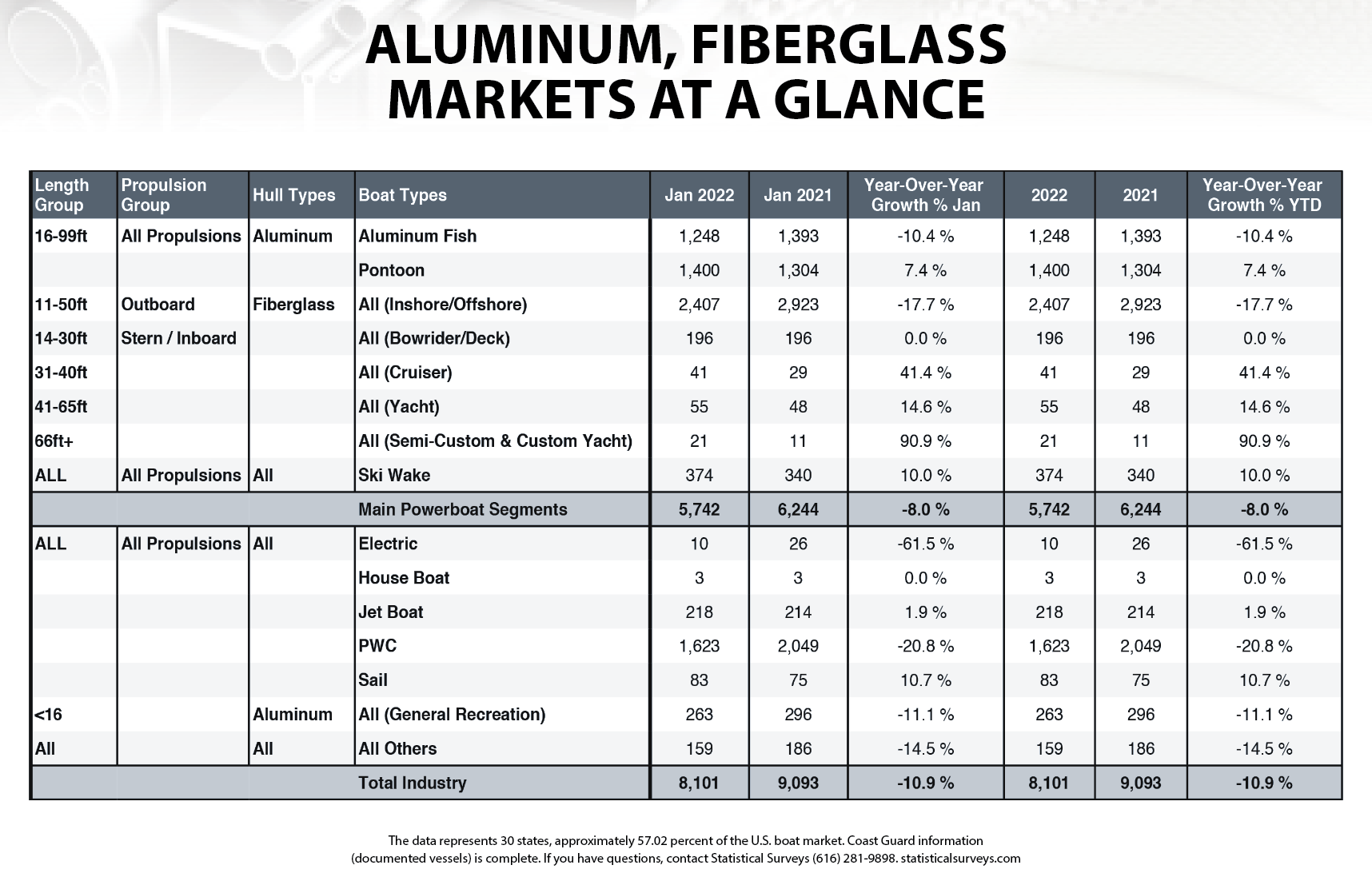

Boat registrations dropped 8 percent in the main powerboat categories in January versus January 2021 as boatbuilders grappled with supply-chain snarls, but robust demand for new boats persisted in a month that typically sees little action.

Boats larger than 31 feet saw the most growth this January, possibly a reflection of strained supply in other categories, with more than 41 cruisers between 31 and 40 feet registered in January, compared with 29 in January 2021, accounting for a 41 percent jump. That’s according to Statistical Surveys, a Michigan firm that tracks new-boat registrations, which revealed preliminary data from 31 states representing about 57 percent of the U.S. market.

Registrations of yachts from 41 to 65 feet grew 14.6 percent year over year, from 48 to 55, and semicustom and custom yachts 66 feet and larger nearly doubled from 11 last January to 21 in January 2022.

Overall registrations were down nearly 11 percent, with the high-volume PWC segment off 20 percent. Overall registrations were also dragged down by a 65 percent drop in the low-volume electric boat sector, which had 10 registrations versus 26 last year.

The largest drag in the main powerboat segments came from fiberglass outboards; the sector, which has remained popular as new-boat demand continues its second year of surge, was down 17.7 percent, with 2,407 registrations in January versus 2,923 the year prior. Aluminum fishing boats had a 10.4 percent dip, with about 150 fewer sold in January this year versus the year prior.

Pontoons and ski and wake boats experienced growth, with a 7.4 percent increase and a 10 percent boost, respectively. Sterndrive and inboard boat registrations were flat after the first year of growth in more than a decade.However, all of those categories except for aluminum fishing were ahead of January 2020, indicating that consumer demand has not waned after spiking during widespread pandemic lockdowns.

Aluminum fishing boat registrations were off 8.1 percent from January 2020, but pontoons were up 57 percent from that timeframe. Ski and wake boats were up nearly 58 percent; sterndrives and inboards grew 32.6 percent versus 2020; and fiberglass outboards grew 4 percent.

That trajectory demonstrates relative demand improvements compared to prepandemic levels, even with supply-chain headwinds at play, according to B. Riley analyst Eric Wold. “As year-over-year comparisons become easier this spring, along with supply-chain pressures beginning to ease into the first half of 2022, we expect the robust consumer demand to become apparent and for this to be better reflected in valuations for the group,” Wold wrote.

In addition, 2020 was the best year the industry has seen for new-boat registrations since 2007, according to SSI sales director Ryan Kloppe.

Two consecutive year-over-year increases in November in December, on top of strong earnings reports from the industry, indicated that boatbuilders could be poised to beat other sectors of U.S. manufacturing in ramping up production. Manufacturers also have robust backlogs and had overwhelmingly positive feedback from the Miami International Boat Show held in February, Wold said.

“As the supply chains likely begin to ease in the second half of 2022, we see a positive setup for the group around improving production/shipment levels and higher average selling prices and gross margins that are not currently reflected in depressed valuation multiples across the board,” he says. “We remain confident these valuation multiple discrepancies will be positively corrected over the next 12 months.”

This article was originally published in the April 2022 issue.