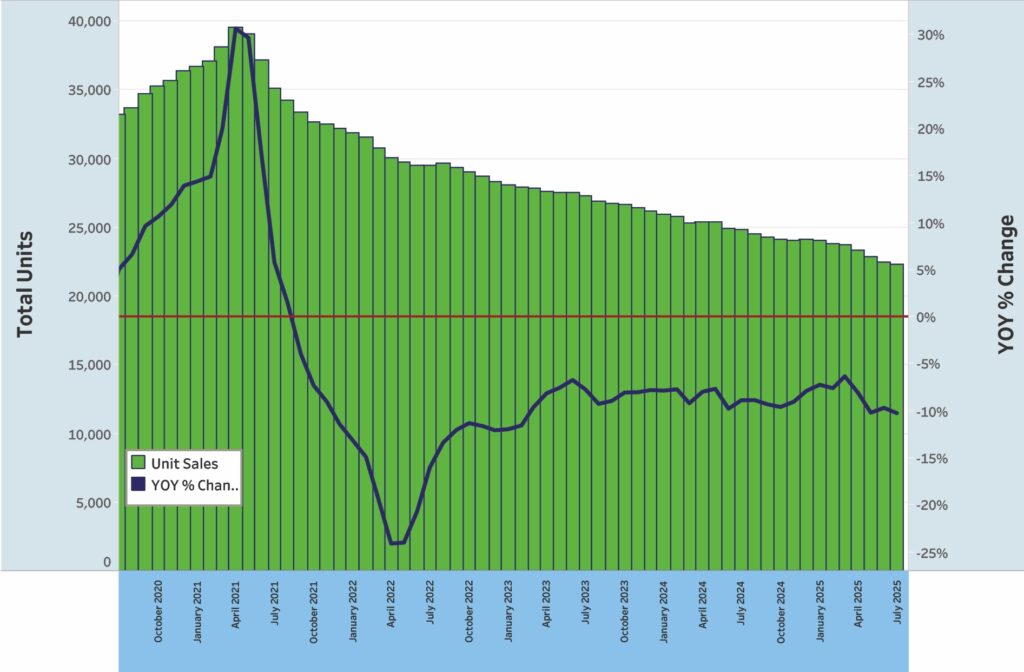

Registration numbers for the 15-foot-and-over U.S. powerboat market were down 7.6% relative to the 12-month rolling average in July. Registrations across all segments totaled 221,055, down slightly from June’s figure of 221,976 units.

The data for new-boat registrations was provided by Info-Link, a Florida-based company that compiles registration numbers from the Coast Guard and individual states.

“While dealers’ payoffs were anemic in April and May, the overall inventory payoffs as a percentage of the total marine loans improved from July through September due to improved sales and the desire of many dealers to reduce floorplan interest and curtailments,” says Russell Baqir Sr., vice president of business development at Northpoint Commercial Financial. “However, the payoffs remain higher than the prior model years as a percentage. An important factor to consider is that the marine market is shrinking, so it’s no surprise that inventory levels continue to decline in keeping with the reduction in demand.

“We also measure marine liquidation ratio, or payoff ratio,” Baqir says, “which is the amount of inventory paid divided by dollar amount of inventory financed. The 2025 ratio YTD has exceeded 2023 and 2024 and was even greater than 2019.”

In terms of the July sales report, the boat category with the steepest decline off 12-month rolling averages was pontoons, down 13.9% for a running total of 48,856 units sold. Runabouts were down 13.2%, with a total of 14,461 units sold, followed by towboats at a 10.8% drop, with 8,088 units on the 12-month average. These reductions are consistent with the continuing downward trend in each respective market.

Only four states showed improvements to their 12-month rolling average of units sold — all of them Western states. Alaska was up 4% year-over-year; California was up 15%; Idaho was up 4%; and Arizona was up 5%. The three largest marine markets, Florida, Texas and Michigan, were all down.

The freshwater fishboat category proved resilient once again in July, with an increase of 1.6% units year-over-year on the 12-month rolling average, and a total of 55,012 units sold. The segment’s three-month rolling average is up 4.2% year-over-year.

“There is an incremental improvement year-over-year in the freshwater market’s inventory turn, thanks in part to reduced inventory in the field compared to 2024,” Baqir says. “As the marine market inventory continues to shrink, inventory turns, and aging will continue improving, though it will not be reflected as a positive on the Info-Link registrations.

“We expect to see continued declines in registrations until supply is balanced with demand in the marketplace,” he adds. “Hopefully, we’ll see increased retail sales activity at [Fort] Lauderdale and into the early 2026 boat shows. On the bright side, dealer interim financial statements are improving, thanks to inventory decline and overall expense reductions.”

Saltwater fishboat sales declined 10.3% below their 12-month averages, for a total of 21,810 units sold. On a three-month basis, the category fell 11.6% for 7,623 units sold. Larger saltwater fishboats also lagged, with vessels larger than 27 feet posting a decrease of 9.1% year-over-year in their 12-month rolling average.

“As a percentage,” Baqir says, “we are seeing the saltwater payoffs improving when compared to 2024, thanks to reduced inventory in the field, which reduced more quickly than other marine segments. We expect this rebound to continue since saltwater has experienced a longer downturn, which should lead to faster inventory turns and decreased aging. Expenses are also declining, contributing to an overall improvement in dealer financial statements.

“Payoffs as a percentage of inventory financed have been relatively positive in the July through September period,” he adds. “I don’t believe the report reflects the impact of the interest-rate reductions across the market yet. Recently, we did hear a Florida dealer sold six boats in one day when the cuts were announced — a significant sales improvement for his dealership over several months. If the Federal Reserve follows through with the projected rate cuts exceeding 1% over the next three to four cycles, we anticipate a very favorable impact on boat sales.”

Baqir says the industry is slowly exiting its recession and expects retail shows to see an uptick in attendance, and a boost in customer demand. He foresees a slight rebound through the 2026 model year. “We are seeing less aged inventory exceeding 12 months and anticipate it should peak and begin to cycle down below 15% of total dealer inventory,” he says.

Manufacturer and dealer sentiments overall appear to be improving, he says. Throughout the industry, manufacturers are investing in R&D, which should result in a flurry of new products in 2026 to entice customers.

“The 2025 year-end financials will reflect improving trends compared to 2024,” Baqir says. “The only dark cloud on the horizon is the anticipated number of dealers that will voluntarily or non-voluntarily exit the industry through the fall and winter months, due in part to inventory liquidation and/or financial insolvency.”