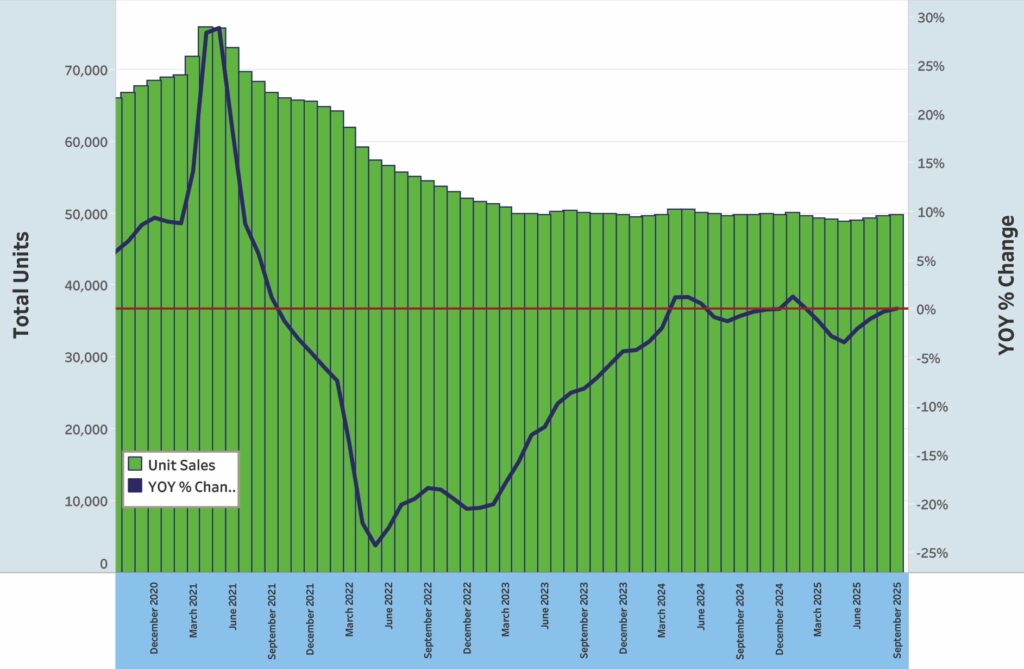

Registration numbers for the 15-foot-and-over U.S. powerboat market in September were 7.1% below the 12-month running average. In units, across all segments, the 12-month running average in September totaled 219,483.

Data for new-boat registrations was provided by Info-Link, a Florida-based company that compiles registration numbers from the Coast Guard and individual states.

“We expect to see high-single-digit declines for the full year 2025,” says Matt Ginsburg, Huntington Distribution Finance’s marine sales leader. “We may see pockets of improvement in various regions and segments, but for the year, the marine retail sales environment will continue its year-over-year declines, and the recent Info-Link data is reflective of this trend.

“We started 2025 with moderate optimism,” Ginsburg adds, “but persistent macroeconomic pressures — such as elevated interest rates and consumer caution — tempered discretionary spending, which directly impacted the marine industry. The broad tariff announcements in Q1 of last year further deflated the optimism that was initially reported at the start of the 2025 retail show season, as widespread initial uncertainty kept potential buyers on the sidelines.”

In the data from the September sales report, the boat category with the steepest decline off its 12-month rolling average was towboats, down 12% for a running total of 7,883 units sold. Pontoons were down 11.8%, with a running total of 48,729 units, followed by runabouts at an 11.5% drop, with 14,409 units on the 12-month average. PWC were down 7% for a 12-month running total of 62,104 units sold.

Freshwater fishboat sales have kept a positive pace, improving for most months in 2025. In September, the 12-month running average was up 0.3% for a total yearly running average of 54,549 units. For the three-month rolling average, freshwater fishboat sales increased 3.9%. The one-month rolling average for that category for September was up 4.6%, showing steadiness through the summer.

“The freshwater fish market continues to outperform broader industry trends, as this segment benefits from a fundamentally different buyer profile,” Ginsburg says. “These units tend to carry a lower overall price point, are often easier to transport and store, and appeal to consumers who view fishing as a core lifestyle activity rather than a discretionary luxury. We continue to see participation in this segment persist even during times of economic uncertainty, leading freshwater fish’s outperformance when compared against other boat segments.”

Saltwater fishboat sales ran 8% below their 12-month averages, for a total of 21,825 units sold on the average. For the rolling three-month running average, essentially the summer sales season, the category was down 2.5%. For the one-month average, saltwater fishboats showed a decline of only 0.1%. Registration numbers for saltwater fishboats 27 feet and larger (inboard and outboard, aluminum and fiberglass) increased in their one-month average in September by 7.1%, with 401 units tallied.

On an overall and state-by-state basis, only two states showed improvements to their 12-month rolling average of units sold: Alaska, up 12% year over year, and California, up 9%. However, on the three-month rolling average, many additional states were up, including Nebraska, Illinois, Louisiana, Alabama, Georgia, North Carolina, Michigan and New York. “The recent uptick in several states is encouraging; however, it likely reflects seasonal buying patterns or favorable, region-specific weather conditions rather than a structural market shift,” Ginsburg says.

“A broader recovery will continue to hinge on key macroeconomic factors: interest rate movements, consumer confidence and inventory normalization. Regional strength in states such as California and Alaska suggests that localized demand drivers, including favorable weather and strong recreational cultures, could create pockets of growth even if the national trend remains flat in early 2026.”

Looking ahead, Ginsburg adds that “we are particularly encouraged by the improvement in overall field inventory, as dealers and OEMs have worked together to reduce aged units and right-size field inventory levels. We fully expect this positive trend to continue and will position the industry well heading into the retail boat-show season.”