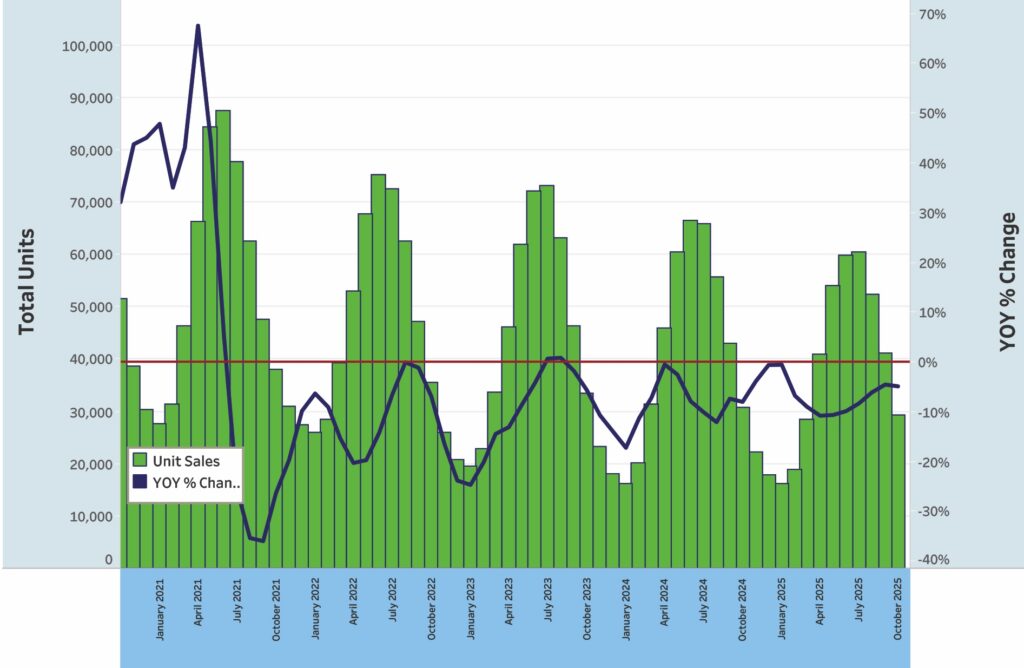

Registration numbers for the 15-foot-and-over U.S. powerboat market through October were down 7.5% relative to the 12-month rolling average. Registrations across all segments totaled 218,292. Aside from a drop seen nearly a year ago due to tariff concerns, sales have trended at roughly this pace for more than a year.

The data for new-boat registrations was provided by Info-Link, a Florida-based company that compiles registration numbers from the Coast Guard and individual states.

Russell Baqir, senior vice president of business development at Northpoint Commercial Finance, says that 2025 “was an incrementally better-performing year in dealer payoffs compared to 2023 and 2024. Dealers’ cash flow improved through this timeframe, and inventory aging overall improved. Dealer financial statements reflect break-even or profit versus 2024, when the majority posted losses. Understanding that registrations are on the decline, dealer inventories are as well. This allows dealer inventory turn to slowly improve as inventory levels trend downward, matching consumer demand.”

In terms of October sales, the category with the steepest decline off its 12-month rolling average was towboats, down 14.2%. Runabouts were down 12.9%, followed by pontoons at a 12.3% drop. These reductions are consistent with the continuing trend in each of their respective markets.

“Dealer inventory turn exceeded market average in the towboat and pontoon segments,” Baqir says. “In these segments, dealer payoffs/liquidations outperformed 2019, 2023 and 2024. The OEMs and dealers have done a good job of reducing field inventory, aligning with consumer demand. These inventory reductions are setting up the dealers for a successful freshwater boat show season. While there remains economic uncertainty, rates are improving to the mid 6%. Given that the 30-year mortgage on homes is now in the low 6% range, retail boat rates are competitive in this environment. Dealer sentiment going into the season remains positive.”

The freshwater fishboat category proved consistent in October with a slight dip from its 12-month rolling average of 0.2% year-over-year, for a total of 54,547 units sold. The segment’s three-month rolling average is up 1.7% year-over-year. Saltwater fishboat sales declined 7.7% below their 12-month averages in October data, for a total of 21,771 units sold. On a three-month basis, the category fell 1.2% for 4,676 units sold. Larger saltwater fishboats also lagged, with models larger than 27 feet posting a decrease of only 0.5% year-over-year in their 12-month rolling average.

About these categories, Baqir says that saltwater and center console payoffs, liquidations and inventory turn “continue to underperform compared to the overall marine portfolio. At the Fort Lauderdale boat show, results were mixed. Some higher-end products exceeded expectations, while the middle-tier and lower-cost products did not meet sales expectations.

“Freshwater fish continued an improving inventory-turn trend,” he adds. “Also, inventory aging in this category has improved below 15% over 365 days, and inventory turn exceeded two times.”

In other categories, PWC sales were off 8.3% from their 12-month rolling average with a total of 61,529 units. The cruiser/yacht category was down 1.7% from its 12-month total with 4,794 units. The unclassified/other category of was up 0.4% with a running average total of 5,216 units sold.

Also, on an overall and state-by-state basis, only Alaska showed improvements to its 12-month rolling average of units sold, up 11% for a total of 860 units on average. Among the larger state markets in October, Michigan was below its 12-month average by 7%; Minnesota was down 6%; Texas was down 6%; and Florida was down 7%. These bigger markets were about on par with the U.S. national average decrease.

As winter boat shows get underway, dealers and manufacturers will be looking for indicators of the market ahead this year. “Although dealer sentiment has been positive,” Baqir says, “the difficulty remains that household consumer debt is at an all-time high, per the Federal Reserve. Also, products in the marine segment are 39% higher in cost than in 2019, continuing the reduction in potential boat buyers. However, dealers and OEMs have continued to focus on reducing the field inventory, and their strategies are working. We should see an incremental improvement in inventory turn and improving gross margins.”

Baqir says a continued focus on inventory reduction and inventory turn should reduce dealership expenses and allow for better gross margins, stable cash flow and reduced inventory aging. “During the 2026 model year,” Baqir says, “marine field inventory should break even with consumer demand.”

This story first appeared in the February, 2026 issue of Soundings Trade Only.