Boat dealers for quite some time have talked about the industry’s numerous challenges the same way chefs list ingredients: inflation, tariffs, interest rates, consumer confidence. It’s often seemed like one problem couldn’t be separated from the next, as if they all blended together into a single, toxic stew.

A good number of dealers and financers are talking differently today. While challenges remain, as of early February, numerous sources told Soundings Trade Only not only that business seems to be looking up, but also specifically that interest rates are no longer one of their main concerns.

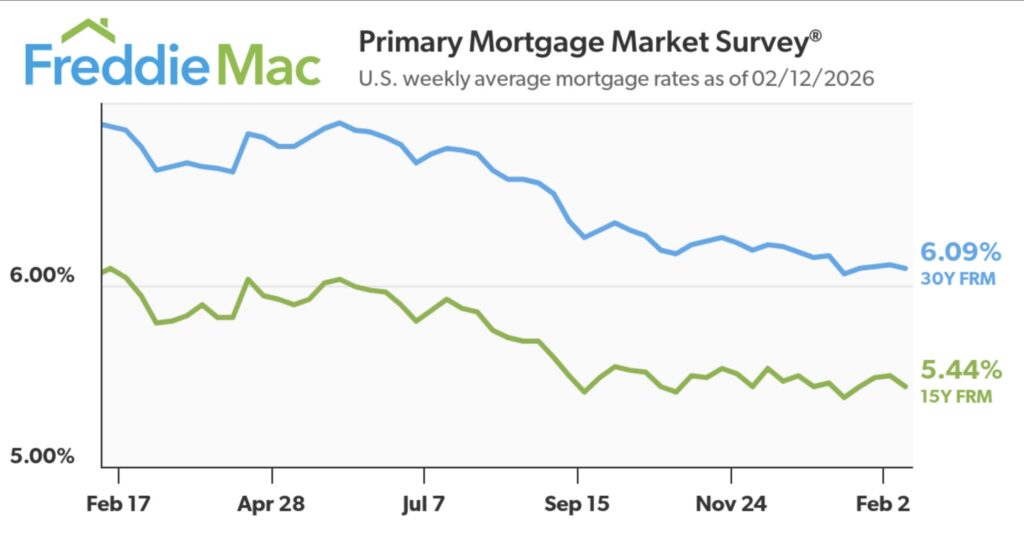

Josh White, principal at Chesapeake Yacht Center in Baltimore, says that for the powerboats his team typically sells in the 40- to 60-foot range, business generally turned around in the fourth quarter of 2025 and was setting up to create a “stellar” year without interest rates being a factor at all. “You can borrow at 5.99 for 20% down right now,” White says. “I don’t think they’re affecting our sales right now whatsoever. Even people who can pay cash are still taking loans because at 5.99, it’s still cheaper than pulling investments out of an account that pays more. It’s not painful at 5.99 compared to where we were.”

Leslie Bott, business manager at Clemons Boats in Sandusky, Ohio, which sells models ranging from about $20,000 to $1 million, says a lot of repeat buyers with good credit are getting rates they can live with, too. “I’d love rates to be lower, obviously, but I don’t think we’re ever going back to where they used to be around 4%,” she says. “A lot of our customers pay cash or have been under 7% this year.”

MarineMax also is seeing customers getting loans and then sealing the deal on purchases — assuming it’s the right type of customer, says Kyle Langbehn, executive vice president and president of retail operations. “On the consumer side, access to financing remains strong overall, but elevated rates can price some potential buyers out of the market or cause them to pause,” Langbehn says. “What we’re seeing is a more deliberate customer, buyers who are taking their time, asking more questions and working closely with our teams to find the right fit.”

“Pent-up demand is starting to come to the table at the boat shows.”

Russell Baqir

Senior VP of business development, Northpoint Commercial FinanceOverall, Russell Baqir, Sr. vice president of business development at Northpoint Commercial Finance, says he’s hearing similar optimism from a lot of dealers who are seeing signs of things looking up this year, especially for qualified buyers who have been waiting to see how things go with the economy. “It’s easy to blame interest rates, and they are a factor that’s taking away the paycheck-to-paycheck guy. It absolutely is,” Baqir says, “but the feedback I’m getting at retail shows is fairly positive. People are out and buying boats right now. It’s nothing that will tell you this year is going to be beautiful, but we’re beating what we did last year.”

Challenges With Trades

Trade-ins are an area where Baqir and others say interest-rate challenges persist. Boats in general cost more today than they did even a half-dozen or so years ago. In 2019, the average invoice he saw for a boat (without an engine) at Northpoint Commercial was around $43,000. Today, he says, the average invoice is about $70,000.

Boats have simply gotten more expensive. And when existing owners want to trade in for a new boat, they’re running into challenges with the way loans are being written today, compared with how banks did business in the past. “A tool that we have historically had available in marine is the buydown,” he says. “You have to look at it like a seven-year ARM on a house. For a few years, you have a good rate that you can afford, and then in year four, you flip to a higher rate, but you had that three years at that lower rate.

“You don’t see those ARMs in the market anymore,” he says. “And in marine, the buydown was eliminated. It’s available to you, but you have to buy down the whole note.”

The buydown used to allow manufacturers — instead of rebating dealers like they’re doing now — to make adjustments and get a deal done, Baqir says. “They used to be able to reduce that interest rate for that teaser period. It’s gone because banks have a significant fear of consumer repos.”

Buydowns weren’t really needed prior to the pandemic, when interest rates were dramatically lower, he says. But with rates now higher and the post-pandemic glut of aging product in the market, the tool would have been hugely helpful. “I have gone and spoken to so many retail finance companies, and I thought I had one that agreed — I was trying to get a buydown that was affordable to go back to the manufacturers and focus on getting inventory moving,” Baqir says. “Nobody wants to do it, and the reason is they’re afraid that if they add this tool back, the consumer will not refi or sell the boat.”

At Sandy Hook Yachts, which sells boats from about $75,000 to about $3.3 million in New Jersey, Connecticut, South Carolina and Florida, managing partner Dan Furnback says the main issue they’re having from an interest-rate perspective is trades. During the pandemic, supply was short, and the company only took in a handful of trades that couldn’t be presold. There was a one- or two-month window to presell each trade before a deal was finalized, limiting the dealership’s exposure to interest-rate issues.

“That’s mostly out the window now. Now we have to take the boat in fully,” Furnback says, adding that because it costs so much to own the trades, the dealership has to offer lower trade-in figures that might not reflect the overall market. That reality, in turn, trickles down and adversely affects new boats.

“The interest rates are higher, and the banks won’t lend you the full amount,” Furnback says. “I had a boat here for a month, so we sold it quickly, but it was a 2022 Sabre 45, and the banks, hypothetically, I got a value of $1.4 million on the boat, but they were only able to lend me $700,000 or $800,000. So that means I pay interest immediately on that $700,000, and I have to come up with the delta and stroke the check to get it done.”

In the past, he says, he might have been able to get a different value, or he could have been out of pocket less by doing things a different way. But today, he says, the banks are “doing it to be on the correct side of it in case people can’t make the payments.” Banks, he emphasizes, are still doing deals, “but they very much want to be on the right side of it.”

Overall Optimism

A key reason for real optimism, several sources say, is that while boats are starting to move again, interest rates are expected to come down even more before the end of this year. It’s possible that there will be two or three interest-rate cuts, based on expectations about President Trump appointing a new Federal Reserve Chairman after Jerome Powell’s term ends in May. “If we can get one in June, that’s good timing,” Baqir says. “And you don’t have to look at the news too much to know Trump is not going to keep him in office. Whoever he brings in, you know he’s bringing rates down at least a percent.”

That doesn’t necessarily mean all kinds of buyers will be able to get back into the boat market, he adds. Building boats is still significantly more expensive than it used to be. For a buyer on the edge of being able to afford the purchase, that problem is not going away. “That monthly payment isn’t just the interest payment,” Baqir says. “It’s also the principal. I can’t go out and buy a million-dollar home without having to readjust the way I live my lifestyle. It’s not necessarily the interest rate that’s prohibitive; it’s also the cost of the product.

“Dealers and manufacturers sometimes say it’s the interest rate, it’s the interest rate, it’s the interest rate, but it’s also a 40% cost increase since 2019,” he adds. “That’s a lot, and costs continue to rise.”

Even so, interest rates coming down may help with the kinds of would-be buyers that White, at Chesapeake Yacht Center, says are having some trouble. “I still have customers that are scrounging to get the 20% down, and their credit is not so great — and yes, it’s harder to get those guys written than it was — but interest rates really haven’t changed the game,” he says. “If anything, they’re getting better. I think there’s more consumer confidence and optimism in where the economy is going. But 5.99 is not a horrible rate for 20 years with 20% down.”

“I don’t think [interest rates are] affecting our sales right now whatsoever. Even people who can pay cash are still taking loans because at 5.99, it’s still cheaper than pulling

investments out of an account that pays more.”

Josh White

Chesapeake Yacht CenterAnd, White adds, selling brands from Groupe Beneteau and Brunswick Corp. gives him advantages on new boats in the pipeline no matter what happens next with interest-rate fluctuations. “I order so far in advance to have these boats built that by the time they came in, if the interest rate was really high, I could probably work something out with the builder,” he says. “Groupe Beneteau offers free flooring for a pretty significant amount of time, so we can sell them without having to worry about getting too deep into interest.” Brunswick does business with him similarly, he says. “Those are two great partners of mine. I consistently order boats.”

Furnback says that for customers taking loans in the 7, 6.99 or 6.59 range, “it’s not far off from a pretty darn healthy economy. But as things get lower, we’re going to spike toward things happening again. The banks will lower value on trades and come at it from a different angle. They’ll still lend, but they’ll lend less. Maybe on a $100,000 trade, they’ll put a value of $80,000 on it. That becomes a cash-flow issue for a business owner. It’s happening now. It’s been going on for the past nine to 12 months.”

And yet business this year is poised for success, Furnback adds. “Interest rates were at their highest around 2024, and then they came down,” he says. “As interest rates came down and I trained our team, 2025 was our best year by 30%, and in 2026 we will crush that by 35% or 40%. It’s strategic planning and thoughtful process, coming up with a stringent approach and sticking to that game plan.”

White is also optimistic about current business conditions. “Things generally turned around in the fourth quarter, and I think it’s setting up to be a stellar year,” he says. “I really do feel like things have made a turn and are heading in the right direction.”

Baqir, too, believes the industry is on the upswing after several years of right-sizing the number of available boats so that inventory is a better match for consumer demand — which includes would-be buyers who are growing tired of watching the economic forecast and waiting for storms to clear. “There’s a guy who works 15-hour days. He loves to fish. His son is the right age. He’s not waiting any longer. He’s buying a boat,” Baqir says. “That kind of pent-up demand is starting to come to the table at the boat shows.

“The aged inventory is coming down,” he adds. “Dealers that are unable to survive, that can’t pay the curtailments or the interest rates, they’re failing. Those boats get pulled back. So the inventory is shrinking to the point that sooner or later, we’re going to meet the demand level. We’re not going to be writing home about what’s happening, but we’ll feel a heck of a lot better than last year. Every year since 2024 is going to feel better and better.”

At the end of the day, Bott says product is indeed moving at Clemons Boats. “We have $20,000 and $30,000 boats, but we also have $500,000 and $1 million boats,” she says. “A lot of those people pay cash. The people who have money still have money.”

This story originally appeared in the March 2026 issue of Soundings Trade Only.