Registration numbers for the 15-foot-and-over U.S. powerboat market were down 10.2% in May from the 12-month rolling average. Registrations across all seven segments totaled 224,976 units on that rolling 12-month basis.

The data for new-boat registrations was provided by Info-Link, a Florida-based company that compiles registration numbers from the U.S. Coast Guard and individual states.

Russell Baqir, Sr., vice president of business development at Northpoint Commercial Finance, told Soundings Trade Only: “May was a step backwards compared to October through April, when each month’s payoffs received by Northpoint exceeded the prior model year’s. According to the University of Michigan, consumer confidence was at a low in April and May ’25. Marine definitely experienced this lack of confidence.”

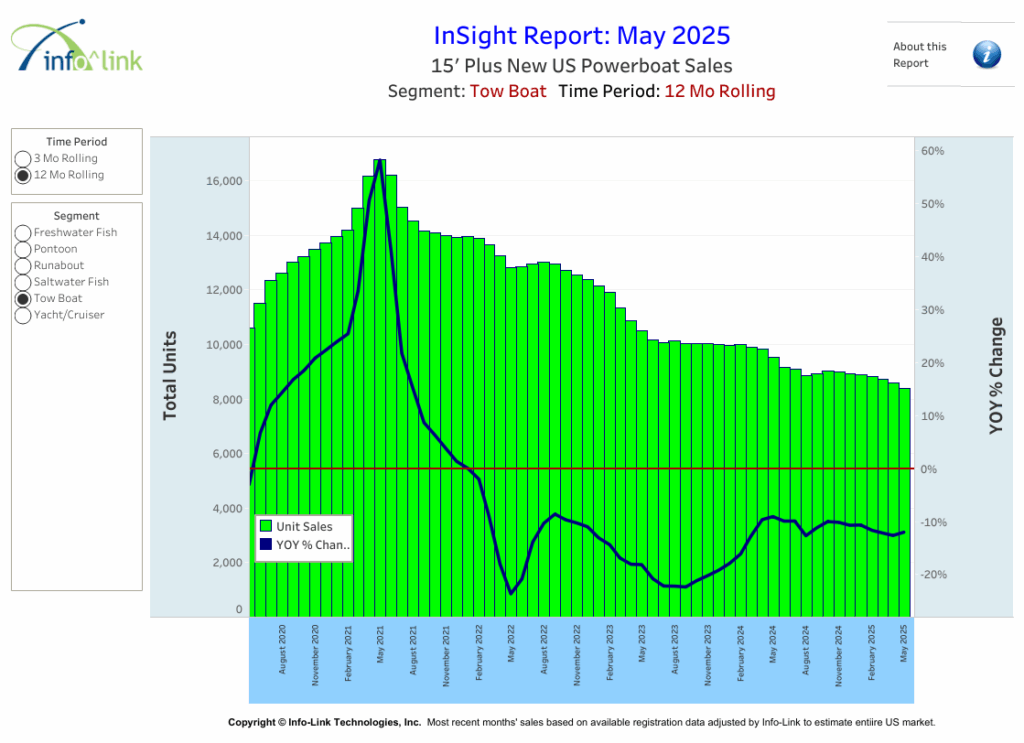

In May, all categories showed declines from their 12-month rolling averages, with the freshwater fish boat segment slowing the least at 0.6% under its 12-month rolling average, with 54,092 units sold. The towboat category ran 11.9% below its 12-month average with 8,378 units sold. Last year’s 12-month rolling average in May for tow boats was 9,509 units.

“According to Northpoint payoffs,” Baqir said, “towboat, freshwater fish and pontoon bucked the trend and outperformed the overall portfolio in payoffs. Floorplan payoffs are typically off from registrations due to timing in the process, but we are seeing positive signs in freshwater segments. The initial feedback has also been positive from the early dealer meetings in the pontoon segment. We have not seen saltwater rebound yet. They entered the slowdown later than the other segments.”

Pontoons were off 15.8% from their rolling 12-month average, with yearly sales on that basis of 50,268 units. PWC were down 10.1% with yearly sales at 64,515 units.

Saltwater fishboat sales ran at 10.5% below their 12-month averages for a total of 22,270 units sold. The cruiser/yacht category was down 4.2% from its 12-month average with 4,857 units. The runabout category posted a 12-month rolling average of 15,315, down 13.3% on a yearly basis.

On a state-by-state basis, Florida was down 13% for a 12-month rolling average of 29,132 boats sold. Texas was down 9% for a 12-month rolling average of 16,483 units. Michigan dropped 9% off its average for 11,778 units sold, and Wisconsin was lower by 13% for a 12-month average of 8,608. Minnesota was down 13% for a 12-month rolling average of 9,534. California dropped 4% for 8,416 units. New York was down 5% with a tally of 8,096 units.

Of the larger states, Pennsylvania showed a 1% gain on its 12-month rolling average with 5,259 units, and Arizona had a 4% gain over its 12-month for 2,831 units.

“We are seeing 2025 calendar year interim financial statements show positive trends compared to 2024 statements,” Baqir said. “However, we continue to see dealers exiting marine by choice or by need. We have also seen dealers refinancing assets to generate cash flow to survive the aged inventory. As we go through the final stages of the down cycle, we are estimating a reduction of dealers by 10% to 15%. The reduction of this capacity and inventory will allow the market/demand to catch up with supply.”

Baqir summed up the recent season by saying: “Floorplan liquidations/payoffs remained slow through the first half of June. July rebounded with a solid payoff trend. The annualized inventory turn improved to 1.48X for the model year ending June 30, 2025, compared to 2024. Also, as stated earlier, dealer sentiment at the initial dealer meetings was positive, and orders were made for the next model year.”