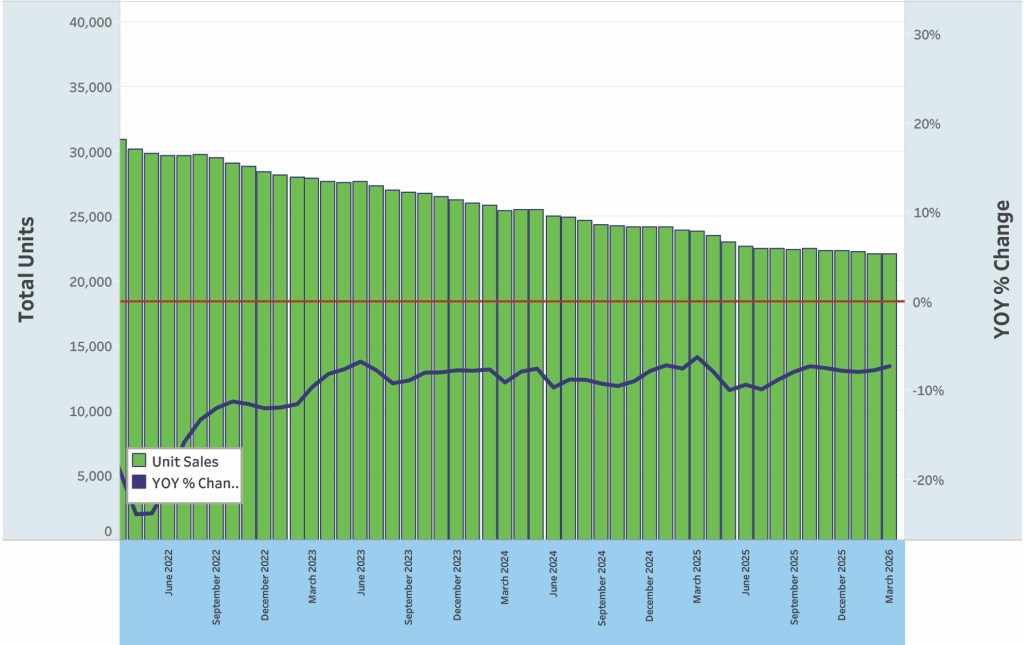

Registration numbers for the 15-foot-and-over U.S. powerboat market through March were down 6.4% relative to the 12-month rolling average. Registrations across all segments totaled 215,445.

The data for new-boat registrations was provided by Info-Link, a Florida-based company that compiles registration numbers from the Coast Guard and individual states.

In the March sales report, towboats were down 11.4% for a running total of 7,802 units sold. Runabouts were down 15.7%, with a total of 13,722 units sold, and pontoons were 10.6% off their 12-month rolling average, with 47,963 units.

The freshwater fishboat category gained 0.5% on its 12-month average in March, with a total of 54,837 units sold. The only other category that showed improvement relative to its 12-month average was the unclassified/other segment, which includes houseboats, foiling boards, airboats and other water sports vehicles. That category showed a 3.1% increase on its 12-month average with 5,113 units sold.

“The market continues to face headwinds stemming from the conflict in Iran impacting consumer confidence and driving higher fuel prices,” says Matt Ginsburg, Huntington Distribution Finance’s marine sales leader. “Freshwater fish remains resilient, given that most buyers in that category pursue their hobby regardless of broader economic conditions, but other segments have continued to show downward trends in retail registrations. That said, we believe boating participation remains solid, and the industry overall has done a fantastic job of finding new ways to reach potential buyers and recalibrate supply with demand.”

PWC sales in March were 11.1% below their 12-month rolling average with 59,812 total units. The cruiser/yacht category was down 6.6% from its 12-month total with 4,632 units. In the March report, saltwater fishboat sales were on a slight rising curve in recent months but still off 7.3% from their 12-month averages, for a total of 21,565 units sold.

Among the bigger state markets in March, Florida was 7% below its 12-month average with 28,237 units yearly. Texas was down 6% with 15,940 units. Michigan was also below its 12-month average by 7% for 11,336 units, while Minnesota was down 9% with 8,976 units. Georgia showed a 1% increase in its 12-month average with 8,250 units.

Other than Georgia, states that showed increases in the 12-month average included Alabama, up 3% with 7,427 boats sold. Idaho was up 11% with 2,020 units on the running figure. Montana had a 1% improvement with 2,008 units. West Virginia was up 6%, and Rhode Island was up 9%.

With the warmer weather and the stock market reaching all-time highs in the spring, Ginsburg says he remains optimistic for the year. He cites new and innovative products to help support retail activity and drive potential new boaters into the market. OEMs and dealers, he says, have done a great job of collaborating to produce marketing content tailored to the next generation of potential buyers, “finding new ways to reach customers that consume content in a completely different way from even just a few years ago.”

Affordability, Ginsburg says, remains the biggest headwind. “Rising fuel prices, higher interest rates, elevated boat prices and tighter consumer liquidity are all weighing on demand at the margin,” he says. “While much improved compared to recent years, dealers are also continuing to work through carryover inventory to ensure their lots are stocked appropriately to match current demand levels.

“Inventory levels are much improved in general but still somewhat elevated relative to current retail demand,” he adds. “Overall, we’re trending toward better balance, but it will likely take more time to fully normalize across the channel.”