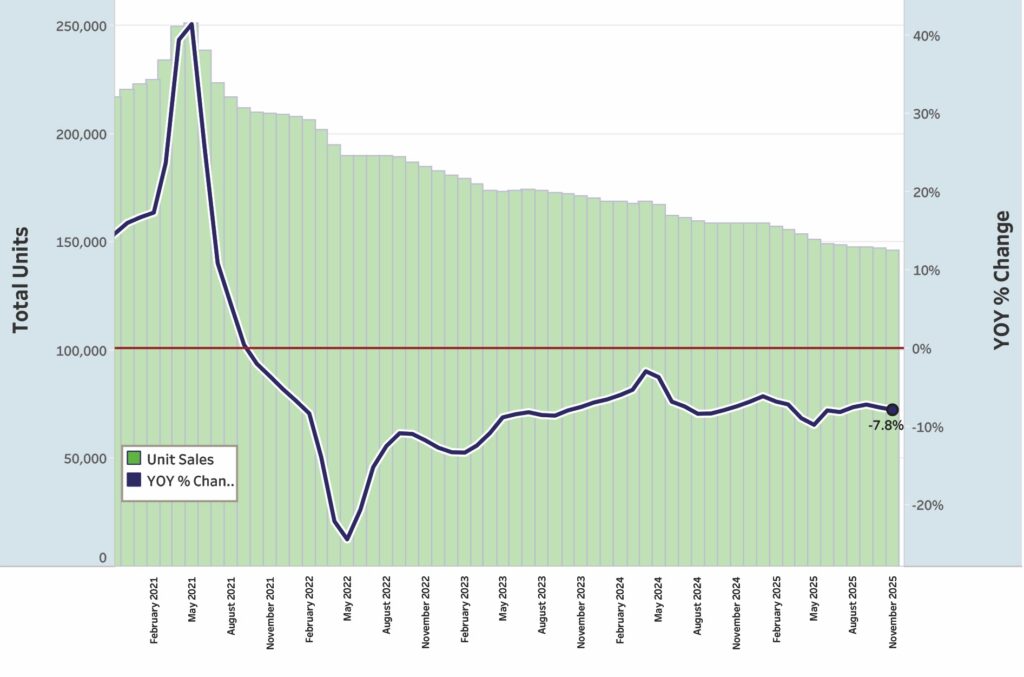

Registrations for the 15-foot-and-over U.S. powerboat market through November were down 7.8% relative to the 12-month rolling average. Registrations across all segments totaled 217,339. Those numbers were roughly on par with the averages of recent months and presented no surprises.

Data for new-boat registrations was provided by Info-Link, a Florida-based company that compiles registration numbers from the Coast Guard and individual states.

“We expect to see similar results in December, as well,” says Matt Ginsburg, Huntington Distribution Finance’s marine sales leader. “While any negative trend can be worrisome, we are not particularly concerned, given that November and December represent such a small proportion of annual retail sales.

“What we’re seeing is really a continuation of the broader trends established throughout 2025, where higher interest rates, uneven consumer confidence and lingering macro pressures weighed on retail activity,” he adds. “We saw the same directional trends through late 2024 and into early 2025. Powerboat sales were running about 9% to 10% below prior-year levels, driven largely by those macroeconomic conditions.”

Retailers have a renewed sense of optimism as 2026 gets going, Ginsburg says. Dealer inventories are much cleaner, and short-term interest rates have come down, improving carrying-cost dynamics and creating a healthier foundation for ordering and stocking decisions.

“This aligns with broader indicators that showed wholesale shipments more closely aligning with retail sales for the first time in years,” Ginsburg says, “a sign the market has been resetting toward more normalized inventory levels. This has led to a much-improved overall dealer sentiment as we entered retail boat-show season.”

In the November sales report, the boat category with the steepest decline off its 12-month rolling averages was towboats, down 14.7% for a running total of 7,709 units sold. Runabouts were down 13.6%, with a total of 14,168 units sold, followed by pontoons at a 12.1% drop, with 48,456 units on the 12-month average.

“Preliminary feedback from retail boat shows thus far has been extremely positive,” Ginsburg says. “Dealers are reporting more engaged buyers and higher levels of sales from retail shows — even at shows where total foot traffic has declined. Dealers are reporting that they are closing more sales or, at minimum, coming away with stronger leads from the retail shows so far, which has been very encouraging to hear.”

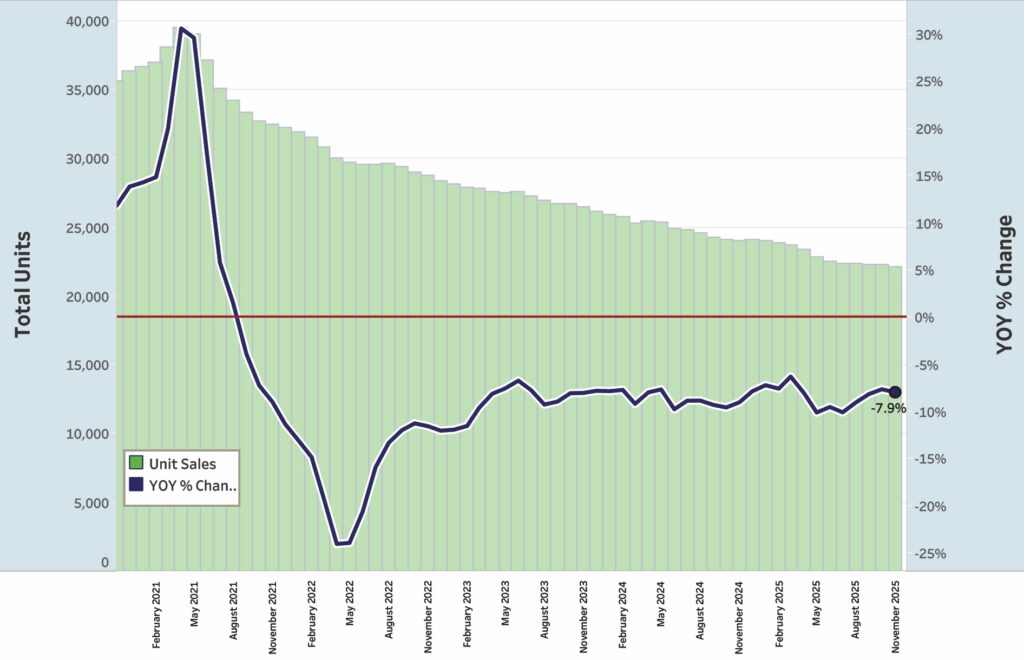

Saltwater fishboat sales declined 7.9% below their 12-month averages in November data, for a total of 21,661 units sold. On a three-month basis, the category fell 4.3% for 3,800 units sold. Larger saltwater fishboats also lagged, with those larger than 27 feet posting a slightly deeper decrease than in recent months of 6.6% year-over-year in their 12-month rolling average. That category of larger saltwater fishboats tallied 5,567 units in the 12-month running average.

The freshwater fishboat category, which was strong most of last year, showed an expected seasonal dip in November from its 12-month average, dropping 1.3% year-over-year, with a total of 54,149 units sold.

In other categories, PWC sales dropped 8.8% from their 12-month rolling average, with a total unit figure of 61,180. The cruiser/yacht category was down 1% from its 12-month total average, with a total of 4,818 units. The unclassified/other category was up 0.2% with a running average total of 5,196 units sold.

On a state-by-state basis in November, Florida was 7% below its 12-month average for 28,649 units. Michigan was also below its 12-month average by 7% with 11,385 units; Minnesota was down 8% with 9,240 units; Wisconsin dropped off 11% for a unit running total of 8,392; New York dropped 8% with 7,751 units; Texas was down 7% with 15,752 units; and California was down by 4% with a total of 7,616 units on the 12-month average. North Carolina was down 3% with 9,794 units. Alaska was the only state showing an increase in November numbers, up 10% on its yearly average of 857 units.

Ginsburg says that, overall, dealer inventories are healthier than at any point in the past three years. Across most segments, he sees stocking levels aligned much more closely with true retail demand, and wholesale shipments have intentionally lagged retail to support this normalization. Foot traffic within dealerships is also reportedly much improved, with fewer tire-kickers and more serious buyers.

“Overall, I would describe the industry as entering 2026 with measured optimism,” he says. “The market has been through an unusually sharp boom-and-cooldown cycle, but the foundational pillars for recovery are falling into place: better inventory balance, improving financing conditions, more stable consumer expectations and positive early boat show activity.

“We still anticipate some variability by segment, but broadly speaking, the industry is healthier, more stable and better-positioned than it was a year ago,” he adds. “The key will be monitoring how consumer confidence, rates and macroeconomic signals trend heading into late Q1, with no surprises like we ran into last year with the broad rollout of tariffs.”

This story originally appeared in the March 2026 issue of Soundings Trade Only.