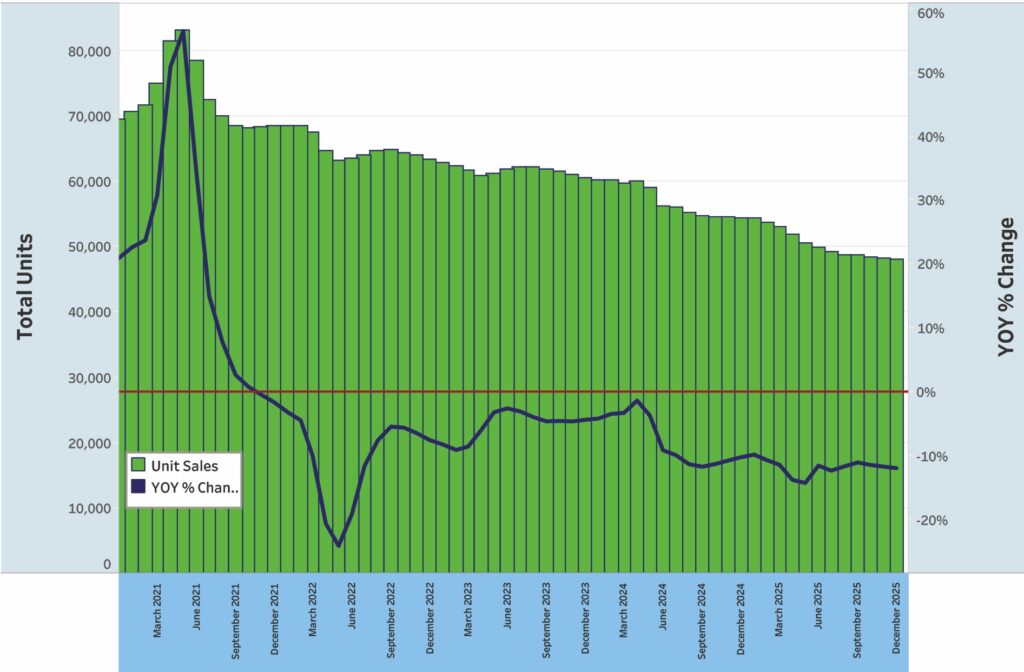

Registration numbers for the 15-foot-and-over U.S. powerboat market through December were down 7.7% relative to the 12-month rolling average. Registrations across all segments totaled 216,988 on the 12-month rolling average. Those numbers were more or less as expected by industry analysts.

The data for new-boat registrations was provided by Info-Link, a Florida-based company that compiles registration numbers from the Coast Guard and individual states.

In the December report, the slower sales season was apparent. Towboats were down 13.8% for a running total of 7,738 units sold. Runabouts were down 14.2%, with a running total of 14,095 units sold, and pontoons were 12.2% off their 12-month average, with 48,322 units on the 12-month average.

“The feedback at the shows reflects good news concerning the freshwater market,” says Russell Baqir, senior vice president of business development at Northpoint Commercial Finance. “Freshwater fish inventory turn continues to outperform all other marine segments. Inventory aging continues to normalize. Pontoon continues an improving trend with payoffs/liquidations as a percentage of portfolio exceeding prior periods during the recession. Pontoon aging over 12 months continues to improve. Similar positive trends are reflected in the towboat market.”

Saltwater fishboat sales were off 8% from their 12-month averages in December data, for a total of 21,656 units sold. Saltwater fishboats 27 feet and larger posted a similar decrease from their 12-month running average, with a decline of 7.8% year-over-year with a unit total of 5,531 units. Saltwater fishboats larger than 33 feet showed a lesser decrease of 6% off the rolling 12-month average, but with 2,107 units sold.

“Overall, saltwater continues to struggle, and aging over 12 months has trended higher than at any point of this current recession,” Baqir says. “Inventory turns have trended to match the slowest performance over recent cycles. However, there are OEMs that continue to perform well through this cycle. Also, feedback at shows projects improving sales figures compared to 2025.”

As much as these numbers may not indicate increases, they do not represent significant drops from averages during the last half of 2025. “There is a stabilization in marine through the continued shrinking of the market as dealers reduce inventory and improve financial performance,” Baqir says. “Overall, the demand for marine products is equalizing to supply.”

The freshwater fishboat category dropped only 1.1% off its 12-month average, with a total of 54,249 units sold. In other categories in December, PWC sales dropped 9.2% from their 12-month rolling average with a total units figure of 60,911. The cruiser/yacht category was down 2.4% from its 12-month total with 4,785 units. The unclassified/other category was up 0.7% with a running average total of 5,231 units sold, an increase from November’s numbers.

On a state-by-state basis in December, Florida was 7% below its 12-month average for 28,540 units yearly. Michigan was also below its 12-month average by 7% for 11,345 units. Minnesota was down by 8% with 9,239 units. These figures were similar to November’s numbers for those states.

In other big markets, Wisconsin dropped off 10% for a unit running total of 8,363; New York dropped 9% with 7,696 units; Texas was down by 7% with 15,765 units; and California was down 5% with a total of 7,602 units on the 12-month average. North Carolina was down only 1% with 9,943 units. South Carolina was off 8% with 6,805 units, and Georgia was down 6% with 8,034 units. Alabama had a drop of 3% with a running average of 7,201 units.

As the industry heads into the spring selling season, Baqir says, feedback has been positive from dealers and OEMs. Inventory levels continue to decrease in each category, aligning closer to demand. “Saltwater has not shown the turn yet, but feedback is positive,” he says. “The expectation in all categories is a reduction of aged inventory through the spring. This trend will set up a greater demand for inventory from OEMs for the 2027 model year.”

Baqir adds, “As the market continues shrinking and capacity reduces to align with consumer demand, mergers and acquisitions of both dealers and OEMs will continue through the 2026 model year.”

This story originally appeared in the April 2026 edition of Soundings Trade Only.