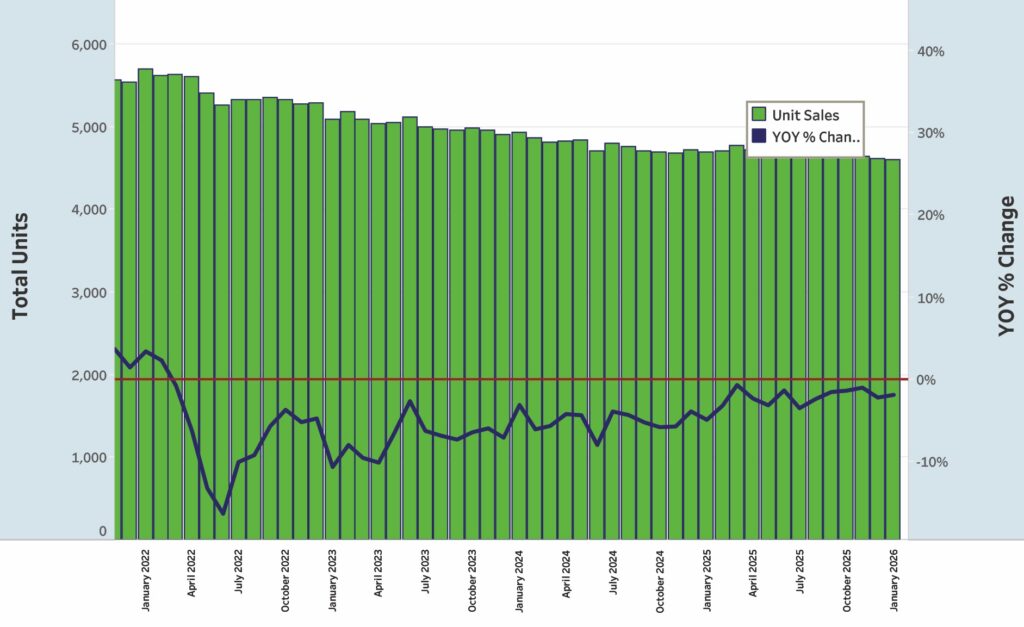

Registration numbers for the 15-foot-and-over U.S. powerboat market through January were down 8.6% relative to the 12-month rolling average. Registrations across all segments totaled 216,398. Those numbers were slightly lower than December’s figures.

The data for new-boat registrations was provided by Info-Link, a Florida-based company that compiles registration numbers from the Coast Guard and individual states.

In the January sales report, towboats were down 13.7% for a running total of 7,758 units sold. Runabouts were down 15.5%, with a total of 13,940 units sold, and pontoons were 12.8% off their 12-month average, with 48,017 units. For comparison purposes regarding pontoons, the January drop represented a decrease of 322 units on the 12-month average compared with the December figure.

“Early winter boat shows had mixed results from a foot-traffic perspective, but dealers and OEMs reported solid lead generation and stronger overall buyer interest, particularly in freshwater fishing and some price-point categories,” says Matt Ginsburg, Huntington Distribution Finance’s marine sales leader. “The shows reinforced that demand is present and bringing out the more serious potential buyers, but decision cycles have clearly lengthened as consumers weigh broader economic uncertainty. The Iran conflict in early March is adding uncertainty and bringing elevated fuel prices, which adds pressure to potential retail sales as we head into prime selling season.”

Saltwater fishboat sales were off 8.1% from their 12-month averages in January — similar to the 8% figure in December data — for a total of 21,586 units sold. Saltwater fishboats 27 feet and larger, posted a decline of 7% year-over-year with a unit total of 5,534 in the 12-month running average. Those numbers are slight upticks from December.

Markets have widely been seen as stabilizing, with expectations of continued inventory reduction in fresh- and saltwater segments, but economic concerns have cast shadows on those expectations. “The stabilization narrative is directionally accurate,” Ginsburg says, “but comes with needed context. Inventories are improving largely because wholesale output has been disciplined, with OEMs conscious of dealers’ historically higher-than-normal inventory levels, not because retail demand has fully rebounded. Demand is steady in the sense that core participation remains strong, yet it is also highly price- and rate-sensitive, relying heavily on strong consumer confidence. We are taking the viewpoint that this is more so the continuation of a controlled reset toward sustainable volumes going forward.”

The freshwater fishboat category dropped only 1.6% off its 12-month average, with a total of 54,496 units sold. In other categories in January, PWC sales dropped 9.9% from their 12-month rolling average with a total units figure of 60,680. The cruiser/yacht category was down 2.2% from its 12-month total with 4,771 units. The unclassified/other category was up 1.2% with a running average total of 5,150 units sold.

On a state-by-state basis in January, Florida was 7% below its 12-month average with 28,556 units yearly. Michigan was also below its 12-month average, by 8%, with 11,315 units. Minnesota was down by 8% with 9,152 units. These figures were all similar to December’s numbers for those states.

Texas was down by 9% with 15,634 units. Louisiana was up 1% with 4,767 units sold on the 12-month average. Alabama was off 3% from its running average for a total of 7,206 units moved. Georgia had a 9% lower average and tallied 7,960 units, and South Carolina was off 7% with 6,823 units. North Carolina was down 1% with a 12-month average of 9,928 units sold.

“Spring should bring seasonal improvement and better conversion of winter boat show leads, particularly in freshwater fishing and entry-level and high-end categories,” Ginsburg says. “However, upside will depend heavily on consumer confidence and overall market conditions, making spring more about incremental gains than a pronounced rebound.

“We are closely monitoring market conditions and trends to start 2026 and remain optimistic regarding stabilization in retail unit sales,” he adds. “The broad industry focus on field inventory levels across the board gives us additional confidence that OEMs and dealers are well-positioned and reacting to retail demand trends.”

This story originally appeared in the May 2026 issue of Soundings Trade Only.