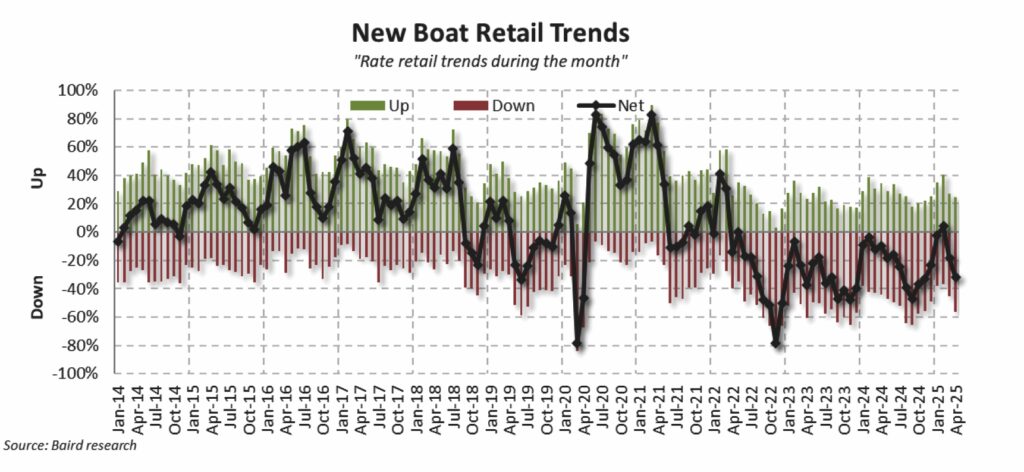

Dealer sentiment on current conditions dropped in April (38 vs. 41 in March), and the three- to five-year outlook dropped (34 vs. 39 in March). These figures were both below the neutral outlook of 50, with dealers continuing to report retail declines in April amid macroeconomic uncertainty and consumer confidence concerns.

For this month’s Pulse Report, Soundings Trade Only, Baird Research and the Marine Retailers Association of the Americas asked 80 marine retailers to assess recent trends in North America. More dealers reported retail declines (56%) than growth (24%) in April, a slight deceleration from March declines (45%) and growth (27%).

Dealers cited tariffs, economic uncertainty, affordability, interest rates, and insufficient incentives and promotions as headwinds to retail demand.

“Unfortunately, pricing seems to be the only thing that is moving boats,” one dealer wrote. “Many other dealers with very heavy inventory around us are heavily discounting units, many at less than 10% gross margins, causing the market of the same brands to lower pricing. Consumers are willing to drive hours to save, so everyone is having to lower pricing.”

Another said: “While some promotions are performing well, others are falling short. Competition remains intense, with minimal margins on sales. We’re strategically matching select prices, but upcoming tariffs will force price increases.”

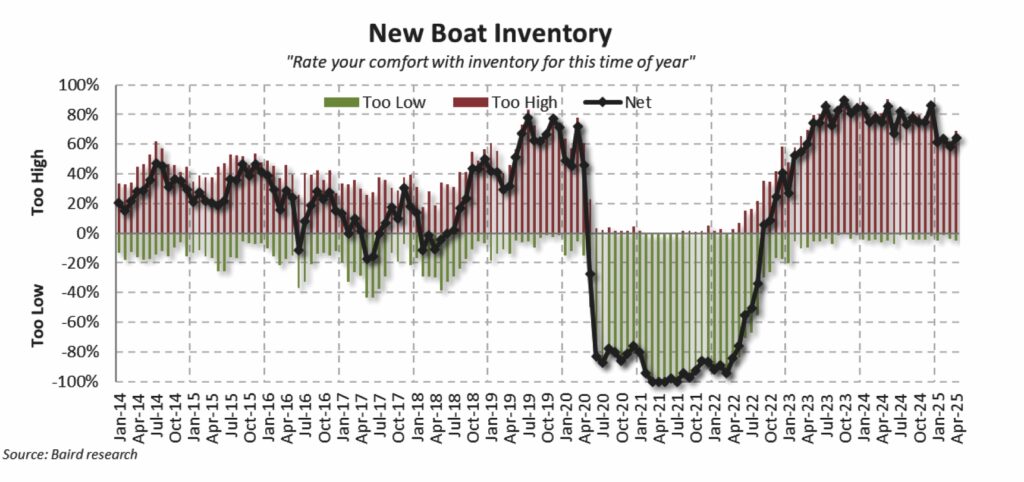

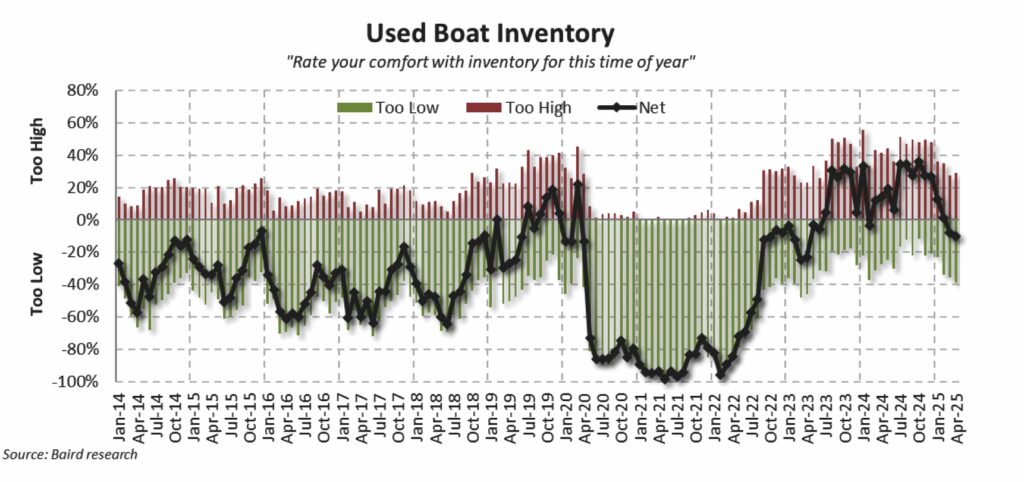

Dealers again reported that new-boat inventory was higher than they prefer. In April, 69% of dealers said new-boat inventory was “too high,” compared to 5% who said “too low.” For used-boat inventory, 39% of dealers reported “too low” compared to 29% who responded “too high.”

When asked what was working, dealers cited social media and, specifically, Facebook Marketplace.

“Facebook and social media appear to be bringing most of the attention,” one wrote. Another said: “Facebook Marketplace since every boat listing service is too expensive and a joke for the money spent.” Another dealer replied: “Grassroots events, customer relationships and leverage referrals.”

When asked what was not working, dealers said costs added by tariffs. One dealer said: “Tariffs are an additional expense which cannot be absorbed. Receiving our first inventory of product with large tariff additions. Additional costs must be passed on.” Another wrote: “Tariffs and playing games with the world supply chain and trade partners.”

The survey also asked dealers about boat orders based on sales performance and OEM expectations. About half of dealers responded that orders were on track to meet requirements, while 35% reported orders below target, and 16% reported boat orders that exceeded requirements.

Dealers also were asked if they planned to increase, decrease or maintain their current order levels for their top brand, and why. One dealer’s comment represented what several said: “I would say the same at the moment, but something has shifted in April that has given me pause. Preowned sales are still strong, but new-boat sales have hit a little bit of a wall in the back half of the month. Through the first four cumulative months, we’re still ahead of last year, but April has been very soft on new activity. And our traditional in-water event is not getting the traction it used to.”

Links to the survey are posted twice monthly on the Soundings Trade Only Today website.